Abstract

The erosion of the liberal international order—marked by WTO/WHO stagnation, protectionism, and supply-chain fragmentation—has constrained Global South access to affordable medicines. While Western “TRIPS-plus” regimes privilege corporate innovation models, India has increasingly leveraged its pharmaceutical sector as an instrument of strategic autonomy.

This paper asks: How does India convert pharmaceutical capacity into geopolitical influence in an emerging multipolar order, and what structural limits constrain this strategy? This paper introduces the original concept of medicinal multipolarity to explain how pharmaceutical production becomes a vehicle of norm-shaping and South-South cooperation. Using qualitative policy analysis of the Economic Survey 2025–26, the BioPharma SHAKTI scheme, and the February 2026 India–Brazil regulatory MoU, the study examines India’s turn toward minilateral health partnerships beyond multilateral gridlock.

The paper argues that India pursues offensive autonomy through regulatory harmonization and biosimilar expansion, seeking to build medicinal corridors across BRICS+ and Latin America. However, this ambition is constrained by a structural “API Paradox”: 70–80% dependence on Chinese Active Pharmaceutical Ingredients and historically low R&D investment (7–8%) limit sovereign innovation capacity.

India’s geopolitical credibility, therefore, depends on transitioning from a low-cost generics supplier to a sovereign biopharmaceutical innovator capable of insulating value chains from both Western protectionism and Chinese supply shocks. The success of this transition will determine whether India’s equity rhetoric translates into durable structural influence in a fragmented global order

Keywords: Medicinal multipolarity, Strategic autonomy, Biopharma Shakti, API Paradox, Global south, Minilateralism

Introduction

The post–Cold War liberal consensus in global health governance has fractured under the weight of great-power competition, institutional paralysis, and protectionist resurgence. Multilateral mechanisms that once facilitated predictable access to medicines increasingly operate amid geopolitical contestation and regulatory fragmentation. Simultaneously, TRIPS-plus disciplines embedded in free trade agreements have narrowed the policy flexibilities that enabled India’s generics revolution, deepening access asymmetries in the Global South.

India occupies a paradoxical position within this reordering. It is the world’s third-largest pharmaceutical producer by volume, with FY25 sector turnover of ₹4.72 lakh crore and exports exhibiting 7% CAGR over FY15–FY25. Yet its structural position remains bifurcated: globally indispensable in generics, but strategically vulnerable in upstream inputs and innovation intensity.

This paper advances medicinal multipolarity as a conceptual framework for understanding how India seeks to convert pharmaceutical capacity into geopolitical leverage. Rather than treating health diplomacy as symbolic soft power, medicinal multipolarity conceptualizes pharmaceuticals as dual-use assets—economic instruments of access and geopolitical tools of production-based institutional balancing. India’s strategy reflects a deliberate attempt to construct autonomy within a multipolar order through regulatory convergence, minilateral alliances, and value-chain fortification. However, endogenous constraints—API concentration and innovation deficits—threaten to undermine this ambition unless addressed decisively.

Literature Review

Existing scholarship highlights the contradictions embedded within global health governance. TRIPS flexibilities facilitated India’s ascent through compulsory licensing and process innovation, yet TRIPS-plus encroachments have progressively constrained those flexibilities. Pandemic disruptions further revealed the fragility of geographically concentrated pharmaceutical supply chains.

Multipolarity scholarship has begun to examine health as a domain of contestation, particularly within BRICS configurations. India’s vaccine diplomacy during COVID-19 illustrated the geopolitical salience of medical supply. However, the literature has insufficiently theorized pharmaceutical ecosystems as systematic instruments of balancing in a post-hegemonic order.

This paper bridges that gap by synthesizing multipolarity theory with health political economy. It reframes India’s pharmaceutical sector not merely as a commercial actor but as a site of production-based institutional balancing—where standards, supply chains, and biosimilar innovation function as strategic resources in contests over regulatory authority and intellectual property norms.

Theoretical Framework: Medicinal Multipolarity

Medicinal multipolarity conceptualizes pharmaceutical capacity as a strategic asset in a fragmented global order. It extends neo-realist balancing logic beyond military domains into regulatory and industrial spheres. Specifically, it constitutes production-based institutional balancing: states leverage domestic productive capacity and regulatory standards to counter hegemonic enclosure without direct confrontation.

Pharmaceutical infrastructure and regulatory credibility operate as hybrid material-institutional assets—simultaneously economic resources and instruments of normative authority. This form of balancing is predominantly soft and institutional: it relies on normative diffusion, epistemic community formation, and standards-setting leverage rather than coercive or military means.

The framework rests on three interlocking pillars:

- Norm-Shaping: Generics and biosimilars function as material critiques of IP maximalism. By sustaining affordable supply, India advances equity as a counter-hegemonic norm embedded in production rather than rhetoric.

- Minilateral Cooperation : Bilateral and plurilateral arrangements (BRICS+, regulatory MoUs) circumvent multilateral paralysis. These minilateral architectures enable selective harmonization outside Western-dominated regulatory pathways.

- 3. Offensive Autonomy : Strategic fortification of upstream inputs and innovation ecosystems reduces vulnerability to coercive interdependence, insulating India’s normative agency from supply shocks.

Credible medicinal multipolarity requires insulation. Without value-chain resilience and innovation capacity, norm advocacy risks degenerating into symbolic positioning. Scope conditions include an established generics base, regulatory credibility, and sufficient scale economies—conditions not universally replicable but potentially adaptable by mid-tier powers.

Empirical Analysis: India’s Policy Pivot

Economic Survey 2025–26

The Survey signals a shift from volume dominance toward value accretion in complex generics and biosimilars. While India maintains volumetric leadership, policy emphasis has pivoted toward innovation-driven growth and global regulatory integration—an explicit recognition that volume alone does not secure strategic autonomy.

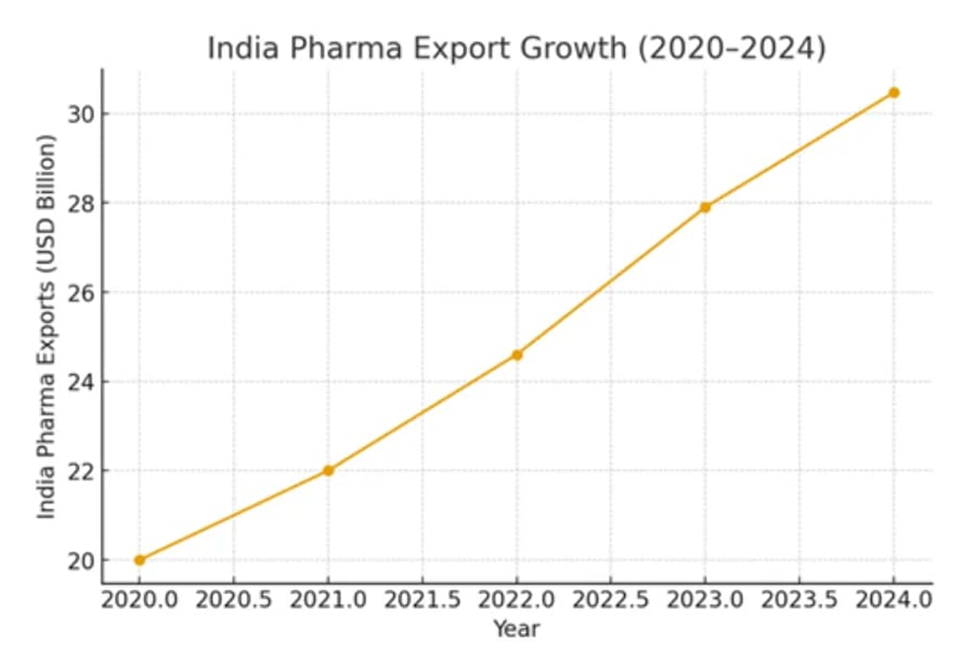

This export growth trajectory (illustrated above) evidences steady escalation, yet underscores the imperative for value-chain ascent amid fragmentation.

Figure 1: India’s Pharmaceutical Export Growth (2020–2024), illustrating the volume-driven base supporting the pivot to value-based autonomy (source: industry analysis, Eminence Group Ventures, 2025).

BioPharma SHAKTI

The 2026–27 Budget introduced BioPharma SHAKTI (₹10,000 crore over five years) to strengthen biologics, biosimilars, clinical infrastructure, and domestic manufacturing. The initiative targets high-burden therapeutic areas such as oncology and diabetes while positioning India to capture value from the 2025–2030 biologics patent cliff (estimated at $236–400 billion in annual revenues at risk globally, variation reflecting differences in firm scope, regional coverage, and product inclusion).

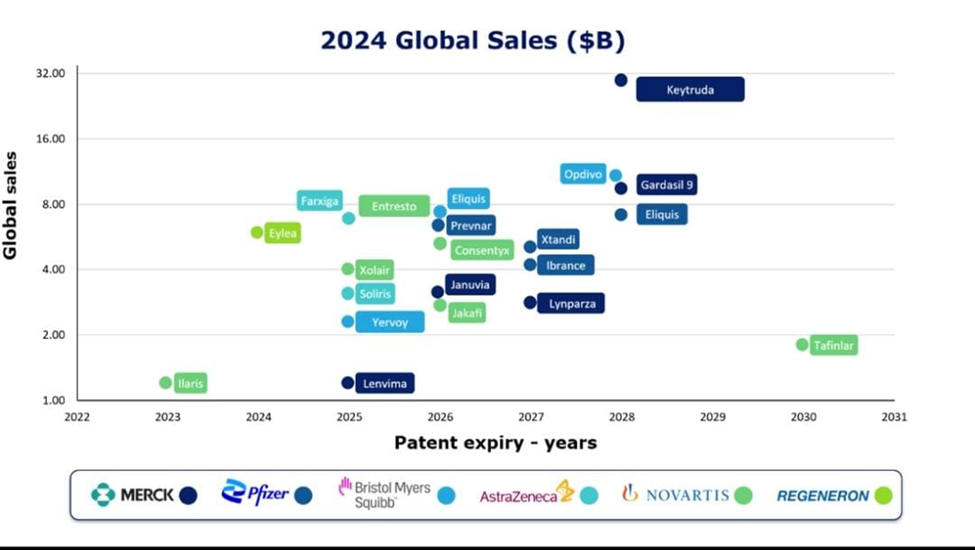

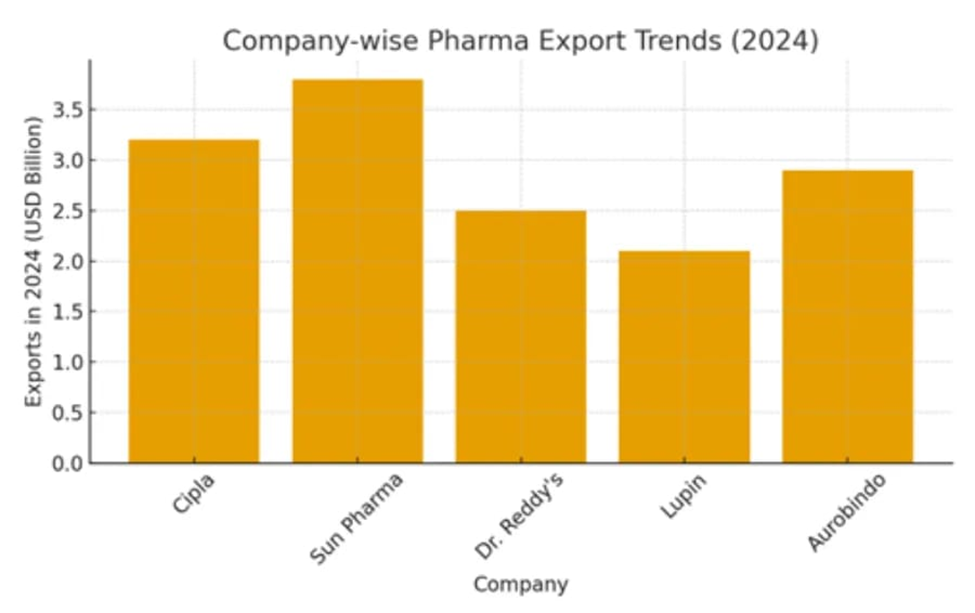

Figure 2: Company-wise Pharmaceutical Export Trends (2024), demonstrating the role of private multinationals in India’s global generics leadership and potential for aligned geopolitical objectives (source: Eminence Group Ventures, 2025).

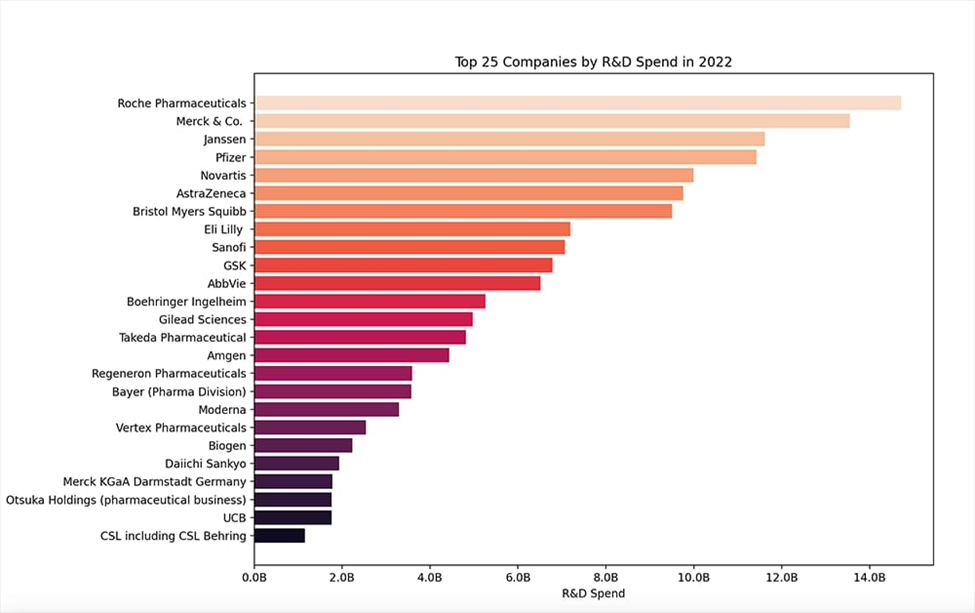

Figure 3: Top 25 Global Pharmaceutical Companies by R&D Expenditure (recent benchmark), highlighting the massive absolute gap that perpetuates India’s generics entrapment and innovation deficit (source: Drug Discovery Trends, 2023–2025 updates).

This marks a transition from reactive generics substitution toward proactive value capture in complex biologics—central to offensive autonomy.

India–Brazil Regulatory MoU (February 2026)

The CDSCO–ANVISA agreement institutionalizes cooperation across pharmaceuticals, biologics, devices, and ingredients through structured regulatory convergence. Rather than relying on FDA/EMA validation, the MoU facilitates South–South standards recognition, lowering non-tariff barriers and integrating supply chains across BRICS+ corridors.

This is medicinal multipolarity operationalized: regulatory harmonization becomes geopolitical infrastructure.

Structural Limits: The API Paradox and Innovation Deficit

The API Paradox

Despite downstream manufacturing strength, India imported approximately USD 4.35 billion in APIs in FY2024–25, with China accounting for 73.71%. In fermentation-based segments—such as penicillin G intermediates—dependence approaches 90%.

This asymmetry creates acute supply-shock vulnerability. While the Production-Linked Incentive (PLI) scheme for bulk drugs has mobilized significant investment and created capacity for 26 critical products, fermentation ecosystems require 3–5 years to stabilize. Autonomy therefore unfolds on a delayed temporal horizon.

The infographic above encapsulates this paradox: manufacturing strengths juxtaposed against Chinese input hegemony.

Low R&D Intensity

Indian pharmaceutical firms allocate 6–8% of revenues to R&D, compared to 15–25% among global majors whose absolute annual expenditures exceed $10 billion. This gap entrenches generics dependence and constrains sovereign innovation, though recent policy emphasis on complex molecules shows gradual upward trends.

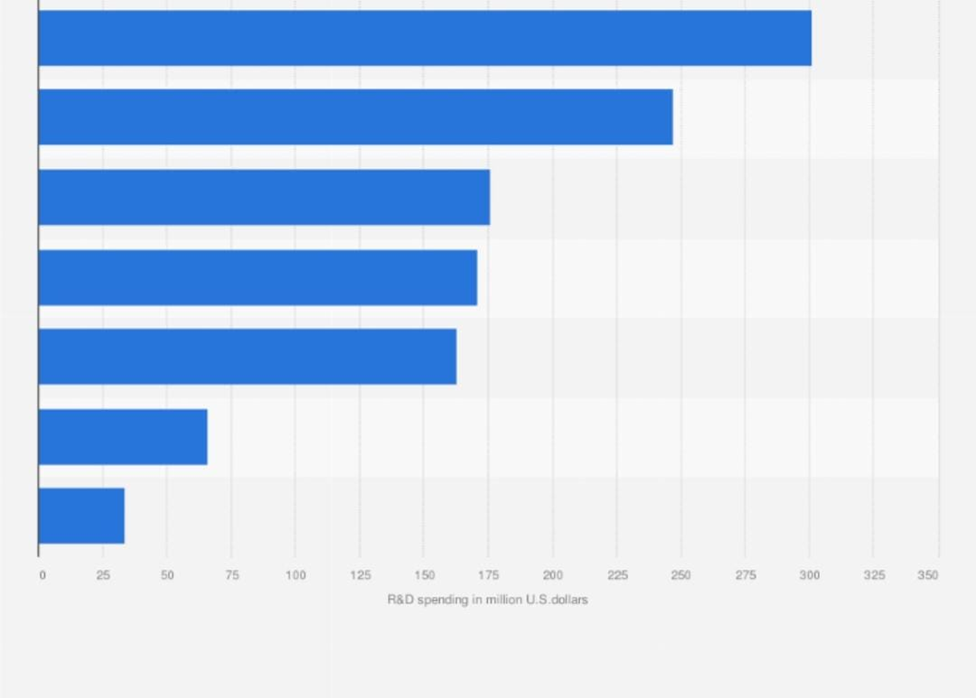

Figure 4: R&D Spending by Top Indian Pharmaceutical Companies (recent data), underscoring the low absolute investment levels constraining sovereign innovation capacity (source: Statista / industry reports, 2025).

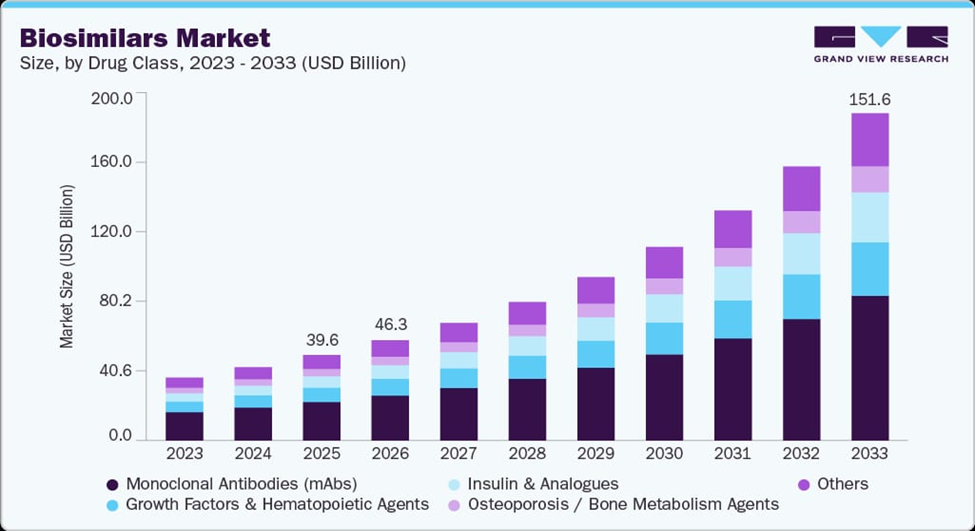

Figure 5: Projected Global Biosimilars Market Growth by Drug Class (2023–2033), illustrating the massive opportunity from the 2025–2030 biologics patent cliff that BioPharma SHAKTI aims to capture for value sovereignty (source: Grand View Research, 2025).

These bar charts dramatize the disparity: global majors’ absolute spends dwarf Indian capacities, perpetuating generics entrapment.

Together, these constraints produce a structural tension: pharmaceutical capacity grants India normative leverage, yet upstream dependence and innovation asymmetry limit the durability of that leverage.

| Constraint | Key Metric | Value | Source | Geopolitical Implication |

| API Dependence on China | Import share (FY2024–25) | 73.71% (of total bulk drugs & intermediates imports, valued at ~USD 4.35 billion) | DGCIS via PIB (2026) | Acute supply-shock vulnerability; risks single-source leverage in geopolitical tensions |

| Strategic APIs | Fermentation segments (e.g., penicillin G KSMs, 6-APA for antibiotics like amoxicillin/cephalosporins) | Up to 90–95% | DrugPatentWatch (2026); ICRA (2025); industry reports | Points of failure in essential antibiotics; undermines health security and sovereign production |

| R&D Intensity | % of revenues (Indian firms average) | 6–8% (projected steady at 6–7% in FY2026) | ICRA (2025–2026); EY–OPPI (2025); company/sector outlooks | Inhibits transition to innovative leader; perpetuates generics trap amid global innovation race |

| Global Benchmark | Big pharma R&D % / Absolute spend | 15–25% / $10B+ per major firm | Industry reports (2025–2026); global benchmarks (e.g., Merck, Novartis analogs) | Widens absolute gap for sovereign innovation; limits norm-shaping capacity in multipolar health order |

Discussion: Competing Models and Counterarguments

India’s medicinal multipolarity contrasts with China’s Health Silk Road, an extension of the Belt and Road Initiative emphasizing infrastructure-embedded bilateralism. China’s model often entails loan-financed facilities and supplier-linked dependencies—what may be termed infrastructure-embedded dependency.

India’s approach instead prioritizes standards-embedded interdependence. Regulatory convergence creates reciprocal market access and institutional linkage without sovereign debt entanglement. Influence emerges through epistemic communities and agenda-setting power rather than infrastructure lock-in.

However, two counterarguments merit consideration.

First, India remains deeply integrated into US and EU export markets and dependent on Western regulatory approvals. This interdependence tempers claims of full autonomy. Yet medicinal multipolarity does not imply autarky; it seeks diversification sufficient to mitigate coercive vulnerability.

Second, India’s pharmaceutical champions are private multinationals driven by profit imperatives. State orchestration is therefore indirect. Nevertheless, industrial policy instruments (PLI, BioPharma SHAKTI, regulatory diplomacy) align private incentives with geopolitical objectives—illustrating embedded autonomy rather than centralized control.

Figure 6: Major Biologics Patent Expiries and Global Sales (2024–2031), highlighting the high-value opportunities and risks during the 2025–2030 patent cliff window (source: industry analysis, 2025).

Conclusion

Medicinal multipolarity illuminates India’s attempt to reposition pharmaceuticals as instruments of production-based institutional balancing within a fragmented order. Through norm-shaping, minilateral cooperation, and offensive autonomy, India seeks to convert generics legacy into strategic leverage.

Yet autonomy remains conditional. The API Paradox and innovation deficit impose structural ceilings that must be overcome to achieve value sovereignty. Transitioning from volume equity to innovation-backed resilience is not merely an industrial upgrade—it is a geopolitical imperative.

If realized, medicinal multipolarity could provide a replicable template for middle powers seeking agency within a multipolar health landscape. If stalled, it risks remaining an aspirational discourse constrained by upstream dependency and technological asymmetry.

In a world where regulatory standards and supply chains increasingly constitute instruments of power, the trajectory of India’s pharmaceutical transformation will shape not only its strategic autonomy, but the contours of Global South agency in the emerging order.

References

Chaudhuri, S. (2020). India’s import dependence on China in pharmaceuticals (RIS Discussion Paper No. 256). Research and Information System for Developing Countries. https://www.ris.org.in/sites/default/files/pdf/DP-256.pdf

Correa, C. M. (2019). Intellectual property and access to medicines: TRIPS flexibilities and TRIPS-plus provisions. South Centre. https://www.southcentre.int/wp-content/uploads/2019/09/TRIPS-Flexibilities-and-TRIPS-Plus-Provisions_EN.pdf

DrugPatentWatch. (2026). Biologics patent expiry and biosimilars market outlook 2025–2030. https://www.drugpatentwatch.com/patent-expiry-biologics-2025-2030

Economic Survey 2025-26. (2026). Economic Survey 2025-26. Ministry of Finance, Government of India. https://www.indiabudget.gov.in/economicsurvey/

Evaluate. (2026). World preview 2025, outlook to 2030. Evaluate Pharma. https://www.evaluate.com/thought-leadership/world-preview-2025-outlook-to-2030

Evenett, S. J., & Fritz, J. (2021). The Covid-19 vaccine production club: Will value chains go global? Global Trade Alert. https://www.globaltradealert.org/reports/62

EY–OPPI. (2025). Indian pharmaceutical industry report 2025. Ernst & Young & Organisation of Pharmaceutical Producers of India. https://www.ey.com/en_in/life-sciences/indian-pharmaceutical-industry-report-2025

Grand View Research. (2025). Biosimilars market size, share & trends analysis report by product, by application, by region, and segment forecasts, 2023–2033. https://www.grandviewresearch.com/industry-analysis/biosimilars-market

Harmer, A., & Buse, K. (2014). The BRICS countries: A new force in global health? Global Public Health, 9(7), 829–835. https://doi.org/10.1080/17441692.2014.935465

ICRA. (2025). Indian pharmaceutical sector outlook. ICRA Ratings. https://www.icra.in/Rating/ShowRationales/Indian-Pharmaceutical-Sector-Outlook-2025

MEA. (2026). India–Brazil Joint Statement and MoU on regulatory cooperation. Ministry of External Affairs, Government of India. https://www.mea.gov.in/bilateral-documents.htm?dtl/38976/IndiaBrazil+Joint+Statement+February+2026

PIB. (2026). India’s dependence on imported APIs: Status and policy response. Press Information Bureau, Government of India. https://pib.gov.in/PressReleasePage.aspx?PRID=1998765

Sell, S. K. (2020). TRIPS-plus provisions in free trade agreements. In D. Halbert & M. David (Eds.), Research handbook on intellectual property and global health (pp. 45–67). Edward Elgar Publishing. https://doi.org/10.4337/9781788113090.00009

Thakur, R. (2022). Vaccine diplomacy and soft power: India’s role in global health. International Affairs, 98(3), 789–810. https://doi.org/10.1093/ia/iiac056

Tribune India. (2026, February 23). India, Brazil sign regulatory pact for pharma and medical devices. The Tribune. https://www.tribuneindia.com/news/nation/india-brazil-sign-regulatory-pact-2026

Wouters, O. J., Shadlen, K. C., Salcher-Konrad, M., Pollard, A. J., Larson, H. J., Teerawattananon, Y., & Jit, M. (2021). Challenges in ensuring global access to COVID-19 vaccines: Production, affordability, allocation, and deployment. The Lancet, 397(10278), 1023–1034. https://doi.org/10.1016/S0140-6736(21)00306-8

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views, positions, or policies of the Jadavpur Association of International Relations (JAIR) or any of their affiliates. JAIR Learning Commons serves as a platform for academic learning and student expression and encourages diverse perspectives and critical engagement.